Every limited company pays corporation tax on its profits. But most directors do not use every legitimate route available to reduce what they owe. Not because they are doing anything wrong, but because nobody has laid it out clearly for them.

This is not about tax avoidance. It is about understanding what the law allows and making sure nothing is missed. The difference between a company that plans its tax position and one that does not can easily run into thousands of pounds each year.

Key takeaways

- Most limited companies can claim more in allowable expenses than they currently do

- Pension contributions made by the company are one of the most tax-efficient ways to reduce your bill

- Dividends do not reduce corporation tax. They come out of post-tax profits, so the timing and structure of how you pay yourself matters

- R&D tax relief remains one of the most underused reliefs available to UK limited companies, including smaller businesses

- Good record keeping is not just good practice. It is what makes every other point on this list actually work

Current Corporation Tax Rates

Before looking at how to reduce your corporation tax bill, it helps to know what rate you are paying.

| Profit Band | Rate | Notes |

|---|---|---|

| Up to £50,000 | 19% | Small profits rate |

| £50,001 to £250,000 | Marginal relief | Tapered between the two rates |

| Over £250,000 | 25% | Main rate |

These thresholds are divided by the number of associated companies your business has. If you have two associated companies, each threshold is halved.

Allowable expenses that reduce your Corporation Tax bill

You can consider a lot of things as deductible expenses, let us talk about the major expenses in detail:

Day to day business expenses

These are the costs your company incurs wholly and exclusively for business purposes. If the expense exists because of the business, it is likely allowable.

Common allowable expenses include:

- Staff salaries, employer National Insurance and pension contributions

- Office rent, business rates and utilities

- Equipment, tools and machinery used for the business

- Software subscriptions and technology costs

- Professional fees including accountancy, legal and consultancy

- Business insurance

- Marketing and advertising costs

- Travel costs that are wholly for business purposes

- Training and professional development directly related to the business

Director salary and employee cost

A director’s salary paid through the company is a deductible expense. This is one of the reasons the salary and dividend combination is a common structure for limited company directors.

Charitable donations

Qualifying cash donations to HMRC-registered charities are fully deductible for corporation tax purposes. Gifts of equipment or stock and certain sponsorship arrangements, may also qualify depending on their nature. The donation must be genuinely charitable and not provide a significant benefit back to your company in return.

Disallowable expenses: What cannot you claim?

Not everything you spend through your company reduces your bill. Below is the list of disallowable expenses:

- Client entertaining and hospitality

- Fines and penalties, including HMRC penalties

- Depreciation of assets (capital allowances are claimed instead)

- Costs that have a personal as well as a business element, unless the personal element can be clearly separated

- Dividends paid to shareholders

Do Dividends reduce Corporation Tax?

No, dividends do not reduce your tax. Dividends are paid out of your company’s post-tax profits. That means it has already been calculated and paid before any dividend is declared. Paying yourself a dividend does not change the amount of tax your company owes.

Why the salary and dividend structure still makes sense?

Even though dividends do not reduce tax, the combination of a low salary and dividends remains tax-efficient for directors because:

- Dividends are taxed at a lower rate than salary income for the individual

- Dividends do not attract National Insurance, either for the company or the director

- A low salary that sits below the National Insurance threshold avoids employer NI for the company while still building a qualifying year for the State Pension (if above the Lower Earnings Limit)

The Lower Earnings Limit is currently £6,396/yr, your salary needs to be at least this amount to earn the qualifying year. Paying up to the Primary Threshold (£12,570/yr) avoids National Insurance entirely for both the company and the director.

What directors should focus on instead?

Rather than trying to reduce corporation tax through dividends, the more effective approach is to:

- Maximise allowable expenses before the tax calculation is made

- Make use of employer pension contributions

- Time significant expenditure strategically within the accounting period

- Use available reliefs such as capital allowances and R&D credits

The tax is calculated on profit. The goal is to reduce that profit legitimately before the calculation happens, not after.

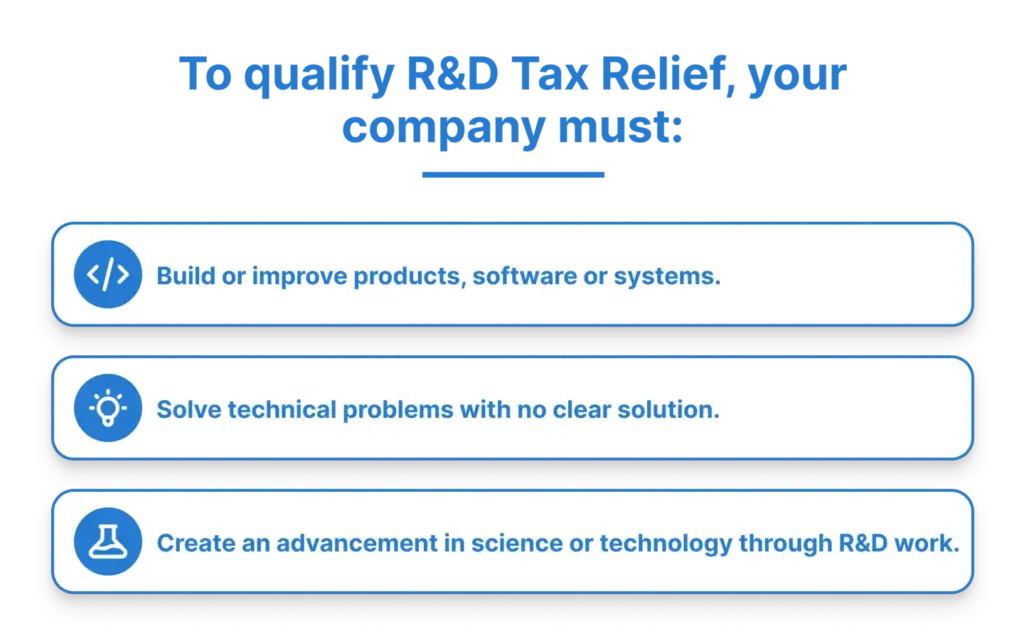

R&D Tax Relief

Research and Development tax relief allows companies to claim an additional deduction against their taxable profits for qualifying R&D expenditure. Most directors who qualify for R&D tax relief never claim it. They assume it’s for labs and tech giants. It is not.

If your company has spent time and money developing a new product, process, software solution, or even an improved internal system where there was genuine technical uncertainty about whether it would work, you may have a qualifying R&D claim.

If any of the following apply to your company, it is worth speaking to a specialist before assuming you do not qualify.

The relief is calculated as a percentage of your qualifying R&D expenditure and reduces your tax liability directly.

What changed from April 2024?

From 1 April 2024, the SME and RDEC schemes merged into one. Most companies now claim a 20% above-the-line credit on qualifying expenditure. A higher rate applies for loss-making SMEs where R&D spending is at least 30% of total expenditure.

If you claimed before April 2024, the old rules no longer apply. Any new claim must follow the merged scheme.

Examples of qualifying R&D work

- A software company solving a technical problem with no ready-made solution

- A manufacturer developing a new production process

- A professional services firm building an internal system with an uncertain outcome

For businesses investing in innovation, R&D tax relief may not be the only available opportunity. Companies that have gone a step further and secured a patent on their work may also qualify for an additional tax benefit through Patent Box.

Patent Box

The Patent Box lets companies pay a reduced 10% corporation tax rate on profits from patented inventions and qualifying IP. It is a separate relief from R&D and a company can claim both at the same time.

To qualify, your company must hold or license a patent from the UK Intellectual Property Office or the European Patent Office and must have been involved in developing that IP. The patent does not have to be a major product. A component, a process, or patented software all count.

Many companies that qualify never claim it. If your company holds a patent or is applying for one, mention it to your accountant.

Specialist reliefs such as R&D tax relief and Patent Box can reduce Corporation Tax significantly for eligible businesses. Beyond claiming available reliefs, broader tax planning decisions can also affect how much tax your company pays and when it becomes due.

Tax planning strategies Directors often overlook

Beyond the core reliefs and deductions, there are several practical tax planning approaches that can make a meaningful difference to your bill. These are not complicated, but they require thinking ahead rather than waiting until after your year-end.

Timing of income and expenditure

Corporation tax is calculated on profits within your accounting period. If you have a large purchase planned, buying it before your year-end rather than after reduces your taxable profit for the current period.

This works because of how capital allowances operate. Depreciation is not deductible for this. Instead, you claim capital allowances on qualifying assets:

- Annual Investment Allowance (AIA): 100% deduction on qualifying plant and machinery, whether new or second-hand, up to £1 million per year.

- Full Expensing: 100% deduction for companies investing in qualifying main rate plant and machinery, with no upper limit. Assets must be new and unused.

- Special Rate First-Year Allowance: 50% deduction for qualifying special rate assets, including long-life assets and certain integral building features. Assets must generally be new and unused

So the timing of a purchase is not just a cash flow decision. It is a tax decision too.

If you expect profits to be higher next year, deferring income where that is commercially sensible can also shift some tax liability into a later period.

Using losses effectively

If your company has made a loss in a previous period, those losses can be carried forward and offset against future profits. Many directors are not aware of how this works or that the option exists. Losses can also in some circumstances be carried back to a previous accounting period, resulting in a refund of corporation tax already paid.

Accounting period

Your choice of accounting period end date can affect how much tax is due and when. This is particularly relevant for companies that experience seasonal variation in income or that are planning significant investment or changes to the business.

For example, a retail business that generates most of its revenue during the holiday season may benefit from choosing a year-end that gives more time to manage cash flow before its Corporation Tax payment is due. Similarly, a company planning to invest in new equipment may be able to align its accounting period to claim available tax reliefs in the most beneficial financial year.

Even small adjustments to timing can support better cash flow planning and make tax liabilities easier to manage.

Structures and group relief

As your business grows, the way your companies are structured can also affect your tax position. If you operate more than one company, group relief may allow losses in one company to be offset against profits in another, reducing the overall Corporation Tax bill.

For example, if one company makes a profit while another in the same group makes a loss, that loss may be used to reduce the taxable profit of the other company. This is a more advanced area of tax planning, but it can be worth discussing with your accountant as your business structure evolves.

When to speak to a Corporation Tax specialist?

Good tax planning is not a one-off exercise done at year-end. It is an ongoing process that works best when your accountant understands your business throughout the year, not just when your accounts need to be filed.

The right time to get advice is:

- Before your year-end, not after, when there is still time to act

- When your profits are growing and your tax bill is becoming more significant

- Before making a large purchase or investment decision

- If you are considering changing your business structure

- If you think you might have a qualifying R&D claim but have never explored it

- When you are planning how to extract profits from the company efficiently

FAQs

What is the difference between tax planning and tax avoidance for a limited company?

Tax planning means using legitimate reliefs, allowances and deductions provided under UK tax rules to reduce your Corporation Tax bill. Whereas tax avoidance is an illegitimate practice that involves artificial arrangements designed mainly to reduce tax in ways HMRC may challenge.

What mistakes cause companies to pay more Corporation Tax than necessary?

Common mistakes include failing to claim all allowable expenses, overlooking available tax reliefs, delaying tax planning until after the year-end and not maintaining proper financial records. These can all lead to missed opportunities to reduce taxable profit.

Can directors reduce overall tax by changing how they take income?

Yes, combining salary, dividends and employer pension contributions can improve overall tax efficiency. While dividends do not reduce Corporation Tax, salary and company pension contributions may help lower the company’s taxable profit.

Does the Annual Investment Allowance apply to second-hand equipment?

Yes, unlike Full Expensing, which applies only to new and unused assets, the Annual Investment Allowance covers both new and second-hand plant and machinery. A company buying used equipment can still claim 100% of the cost against taxable profits in the year of purchase, up to the £1 million annual limit.

Can a limited company claim tax relief on a director’s training costs?

Yes, if the training is directly related to the director’s current role or improves skills used in the business. The cost is treated as an allowable expense and reduces taxable profit. Training for an entirely new trade or profession does not qualify, as it goes beyond the scope of the existing business.

Can a loss-making company still claim R&D relief?

Yes, some loss-making companies may still qualify for R&D support if they meet the eligibility rules. In certain cases, the relief can provide a payable credit even when no Corporation Tax is due.

How often should companies review their tax position during the year?

It is worth reviewing your tax position regularly, ideally every quarter and before your year-end. This gives enough time to plan expenses, check relief eligibility and act on tax-saving opportunities before deadlines pass.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.