A 1263L tax code replacing 1257L rarely comes with an explanation. Your salary stays the same, your employer may not mention the change, and the only visible difference on your payslip is the PAYE tax code.

The change means your tax-free allowance has increased from £12,570 to £12,630. This does not mean HMRC has increased the standard Personal Allowance. Instead, it can reflect £60 of approved tax relief added to your allowance, such as a flat rate expense for work-related costs like uniforms, work clothing and tools under HMRC rules. Until you know why, it’s difficult to tell whether the code is correct or simply carrying forward relief from an earlier job.

This guide explains what the 1263L tax code means, why the extra £60 has been added, how it affects your pay, and how to check whether the code is correct.

Key takeaways

- A 1263L tax code gives a tax-free amount of £12,630 for that job, which is £60 higher than the standard 1257L code.

- One common reason for an extra £60 is an HMRC-approved flat rate expense for uniforms, work clothing and tools, but other adjustments can also change a code.

- HMRC may apply this relief automatically, so seeing 1263L doesn’t always mean a claim has been submitted.

- A 1263L code isn’t always correct. If you’ve changed jobs or your circumstances have changed, it’s worth checking whether the extra allowance still applies.

- The quickest way to confirm why you’ve been given 1263L is by checking your Notice of Coding or Personal Tax Account.

What is the 1263L Tax Code meaning?

Every UK PAYE tax code is made up of a number and a letter and each part has a different purpose.

The number, multiplied by ten, gives the tax-free Personal Allowance for that job. So, 1257L reflects the standard allowance of £12,570, while 1263L reflects £12,630, an increase of £60.

The letter L shows that the standard Personal Allowance applies, with no other adjustment affecting it, according to GOV.UK’s guide to what a tax code means.

This same logic explains tax code letters and numbers generally, not just this one code: the number always gives the allowance and the letter always gives the rule set attached to it.

Understanding what the code means is only the first step. It tells you how much tax-free allowance has been applied, but it doesn’t explain why that allowance has changed. That’s where most of the confusion around 1263L begins.

Is the 1263L Tax Code Good or Bad?

On its own, 1263L is neither good nor bad. It just means £60 has been added to your normal Personal Allowance. Whether that’s good news depends on one simple question: are you meant to have it?

- If you are entitled to it, the code is correct and you get a small tax saving each year.

- If you are not entitled to it, the code isn’t doing you any favours. You are underpaying tax without knowing it and HMRC will collect the difference later.

So the code itself doesn’t tell you anything good or bad. What matters is whether the £60 behind it is real.

Whether 1263L is beneficial becomes clearer by looking at how the extra £60 Personal Allowance affects the amount of tax deducted from your pay.

How 1263L Tax Code affects Take-Home Pay?

The extra £60 of tax-free Personal Allowance doesn’t increase take-home pay by £60. Instead, it reduces the amount of income on which tax is charged, so the actual saving depends on the rate of tax you pay.

HMRC’s guidance confirms this with a worked example: someone claiming a flat rate expense of £60 who pays tax at 20% in that year pays £12 less tax. The same logic scales at other rates, so a higher-rate taxpayer paying 40% would save £24 instead.

How much Tax someone actually pays on a 1263L Tax Code?

The exact saving depends on income, since the £60 is only ever taxed at whatever rate applies to that portion of earnings.

| Category | 1257L | 1263L | Difference |

|---|---|---|---|

| Tax-free allowance | £12,570 | £12,630 | £60 |

| Basic rate taxpayer (20%) | £0 saving | £12 a year, £1 a month | £12 a year |

| Higher rate taxpayer (40%) | £0 saving | £24 a year, £2 a month | £24 a year |

| Additional rate taxpayer (45%) | £0 saving | £27 a year, £2.25 a month | £27 a year |

To put that into context, someone earning £30,000 a year would see the amount of income taxed at the basic rate fall from £17,430 to £17,370. The saving is relatively small on each payslip, which is why many people don’t realise their tax code has changed until they check it themselves.

Are you actually eligible for the extra £60?

Uniform-related flat rate expenses are a common reason for a 1263L tax code, but not everyone qualifies for them. In general, the relief only applies where all of the following are true:

- The employer requires a recognisable uniform or specialist clothing that identifies the job, not everyday clothing worn under a dress code

- The cost of cleaning, repairing or replacing it comes out of the employee’s own pocket, with no free laundering service or reimbursement available

- Protective equipment is handled separately: employers must provide PPE free or reimburse its cost, so PPE itself doesn’t qualify for this relief

Meeting these conditions is what makes someone eligible to claim tax relief for uniforms and work clothing. The specific £60 rate and any higher industry rate, is confirmed separately on HMRC’s list of agreed flat rate expenses by occupation.

This is why work uniform tax relief in the UK is only available in specific circumstances rather than to everyone who wears work clothing.

That doesn’t necessarily mean the 1263L tax code is incorrect. A professional subscription or an automatic coding review can add the same £60 without any uniform being involved at all.

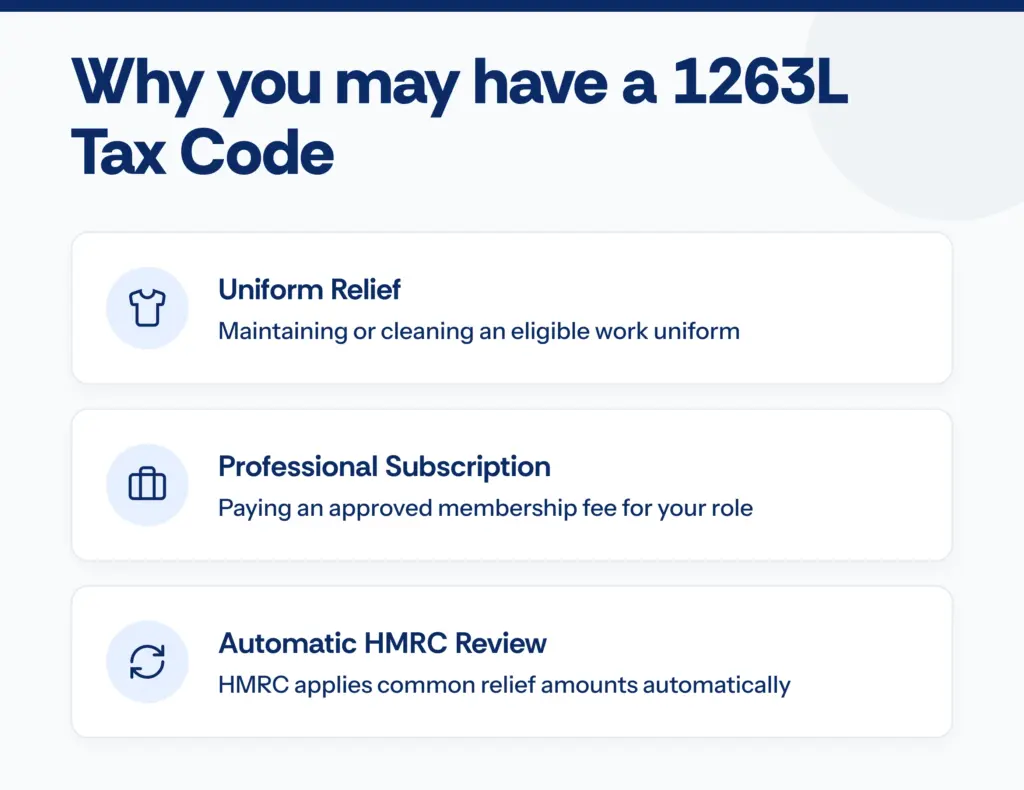

Why HMRC has given you this Tax Code?

The legal basis for flat rate expenses comes from Section 367 ITEPA 2003, which sets the average annual cost of maintaining tools or work clothing for a job. Three reasons explain almost every case of 1263L: uniform relief itself, a professional subscription or HMRC applying the relief automatically.

Uniform and Protective Clothing

Where an occupation has its own agreed rate, that figure replaces the standard £60 rather than adding to it. If an employer already pays toward the cost, only the remaining difference can be claimed.

| Occupation | Annual flat rate |

|---|---|

| No specific industry agreement | £60 |

| Nurses, midwives and most other clinical and care roles | £125 |

| Ambulance staff on active service | £185 |

| Police officers up to Chief Inspector | £140 |

These figures come from the flat-rate expenses list by industry and job. A code of 1263L points specifically to the £60 rate, since 1257 plus 60 makes 1263.

A nurse whose only adjustment is the £125 clinical rate would carry 1382L. Ambulance staff with only the £185 rate would carry 1442L. Other deductions on the same code, such as benefits in kind or underpaid tax from a previous year, would shift the number further.

Professional Subscriptions to an Approved Body

Where uniform relief doesn’t fit, a subscription to an approved professional body often does, provided membership is required for the job. This route works the opposite way to uniform relief. The flat rate needs no receipts, but a subscription claim does.

An Automatic Coding Review

Where neither of those fits, the most likely explanation is that HMRC applied the relief on its own initiative, without an individual claim being made, where an employee’s industry and occupation already appear on an agreed list.

That’s exactly why some people see 1263L without remembering having claimed anything at all. Marriage Allowance is sometimes mentioned as another possible cause, but it changes the code letter itself to M or N rather than adding to the number, so a code ending in L was never affected by it.

Whichever of the three applies, the relief isn’t paid separately. It’s built into the tax code once approved, lowering the tax taken from pay automatically each month. HMRC confirms the change through a Notice of Coding sent separately from the payslip itself.

Reading the Notice of Coding

The Notice of Coding, or form P2, is the letter HMRC sends whenever a tax code changes and it shows exactly what makes up the new allowance. It states the reason in HMRC’s own terminology, such as “flat rate job expenses,” rather than naming uniform relief directly, which is often why the letter raises more questions than it answers.

HMRC is moving away from paper P2 letters for many taxpayers. Instead, they get a digital notification through the HMRC app or Personal Tax Account. Check there directly rather than waiting for a letter to arrive by post.

The three reasons above cover most people who see this code. A smaller group reach 1263L through a change of employer, a second uniformed job, a short contract or a move abroad, none of which involve a fresh uniform or subscription claim at all.

When a different situation explains the Code?

The three causes above account for most people who see this code. Five other situations explain the rest, each tied to a change in circumstances rather than a fresh claim.

- Changed employer mid-year: HMRC confirms that if a new employer doesn’t have someone’s previous income and tax details, they’ll be paid using an emergency tax code until this is resolved, so a 1263L code from a previous job can carry over automatically, whether or not the new role still qualifies for the same relief.

- Working two jobs at once: Uniform relief applies per employment, not per person, so a second uniformed job can, in principle, be claimed separately.

- The code has gone down instead of up: This isn’t covered by anything above. A lower code usually points to a benefit in kind or unpaid tax being collected instead.

- Short-term or seasonal contract: The job can end before HMRC finishes processing a claim, leaving the code unchanged for its entire length.

- Moving abroad partway through the year: Leaving UK employment doesn’t remove a uniform-based code on its own. It needs to be reported the same way a job change does.

Scottish and emergency code variants

Two variations are worth knowing about separately. A code starting with S, such as S1263L, means the same £12,630 allowance applies, but under Scottish Income Tax rates rather than the rest of the UK’s, since Scotland sets its own bands.

A code ending in W1 or M1 (for example 1263L W1) can indicate the tax code is being applied on a non-cumulative basis for that pay period rather than being calculated across the tax year. If this appears, check your PAYE notice of coding and Personal Tax Account for the reason.

A note for Self-Employers

1263L only applies to PAYE income taxed through an employer. Self-employed income runs through Self Assessment instead, using allowable expenses and reliefs claimed directly on the return.

A quick check of the Personal Tax Account still confirms exactly what’s been applied and why, the same way it does for the three main causes.

Does the Relief Disappear if the Job Changes?

Not automatically and that’s important to know before assuming an outdated code will correct itself.

HMRC’s PAYE manual on coding deductions and expenses confirms this directly: when an employment ends, the flat rate expense stays in the tax code for the current year and is only removed the following year if the nature of the employment has changed or can’t be confirmed as broadly the same.

A practical example

Someone moving from a uniformed hospitality role into an office job, for instance, will usually keep the 1263L code untouched through the rest of that tax year.

They carry on receiving relief for a uniform they no longer wear and nothing flags it, because HMRC’s default is to leave the figure exactly where it was until the next review.

What changes from 2026/27

Starting with the 2026/27 tax year, this default no longer holds in every case. According to the Chartered Institute of Taxation, confirmed separately by the Chartered Institute of Payroll Professionals.

HMRC now automatically reviews and can remove any employment expense coded above £120. The standard £60 uniform relief behind a 1263L code sits below this threshold, so it isn’t caught by this change.

The occupation-specific rates for nurses (£125) and ambulance staff (£185) are affected, though, since both exceed £120. HMRC removes the expense if any of these apply:

- The person has no current PAYE income

- There has been a full tax year’s gap in employment since the expense was first claimed

- No Self Assessment return has been filed since 2021/22, despite indicators one was needed

- The coded amount is higher than what was declared on a 2022/23 Self Assessment return

Where this applies, a long-standing 1382L or 1442L code can reset to 1257L even with no real change in circumstances. HMRC does not restore the relief automatically. The person has to resubmit the claim themselves.

If HMRC corrects a code

If HMRC later finds the relief no longer applies, the code is corrected from that point forward and the earlier period stays exactly as it was, with no adjustment made after the fact.

HMRC Tax Code Check: How to Check if your 1263L Tax Code is Correct?

Checking a 1263L tax code takes four steps: opening the Personal Tax Account, confirming a uniform expense, confirming a subscription instead and calling HMRC if neither explains it.

- Open the Personal Tax Account: Sign in on GOV.UK and check what actually makes up the £12,630, not just the code itself.

- Check for a uniform expense: Confirm whether the reason relates to washing, repairing or replacing a work uniform without reimbursement.

- Check for a subscription instead: If uniform relief doesn’t fit, check whether a required professional subscription to a body on HMRC’s approved list explains it.

- Contact HMRC if neither fits: If none of these explanations apply, contact HMRC’s Income Tax enquiries contact page (telephone: 0300 200 3300) to confirm what the additional £60 relates to.

Two people can reach the same code through entirely different routes. A care worker who has never personally contacted HMRC might find the account confirms the standard uniform rate, applied automatically once the employer’s occupation data was on record.

An office worker with no uniform at all might instead find the £60 is coded against a professional subscription they paid without realising it carried tax relief. Keeping the renewal receipt on file is worth doing in that case, in case HMRC asks for it later.

What happens if the 1263L tax code is wrong?

An incorrect 1263L tax code does not always create an immediate problem, but leaving it unchanged can mean the wrong amount of tax is collected over several pay periods.

There are three common outcomes:

- The extra £60 no longer applies: Too little tax is deducted. HMRC usually finds this through a P800 tax calculation issued after the tax year ends, then recovers the difference by adjusting a later tax code. This route only applies to underpayments under £3,000. Above that, HMRC collects it through Self Assessment or a direct payment instead.

- The extra £60 should have been included: Once HMRC updates the tax code, any extra tax paid is normally refunded through PAYE or directly by HMRC. You can claim back overpaid tax for the current tax year plus the 4 previous ones.

- The code is correct: If the additional £60 reflects an approved relief that still applies, nothing further needs to be done.

Employers cannot change a tax code themselves. They apply the code issued by HMRC. If the code is wrong, HMRC must update the record before the new code appears on a future payslip.

How to Claim Uniform Tax Relief from HMRC?

Claiming uniform tax relief from HMRC takes four steps: checking the rate, submitting the claim, covering past years and letting HMRC update the code.

- Check the rate: Use HMRC’s list of flat rate expenses by industry and job to see if the occupation qualifies for a rate above £60.

- Submit the claim: Claim online or by post using form P87 if total employment expenses are £2,500 or less; above that, a Self Assessment tax return is needed instead.

- Cover past years: A claim can cover the current tax year plus the 4 previous ones in a single submission, so someone who’s been washing a work uniform for years without claiming anything hasn’t lost that relief permanently.

- Let it take effect: Once approved, HMRC updates the code going forward. Backdated years are repaid separately, not through the code.

This process is the same whether you’re claiming washing uniform tax relief or another eligible flat-rate expense.

One detail worth knowing before submitting a claim for a work uniform: Since 14 October 2024, HMRC has required supporting evidence for most standalone job-expense claims, such as professional subscriptions, mileage and working from home.

Flat-rate uniform and tool claims are the specific exception. HMRC has confirmed these need no evidence at the point of claiming. It still runs background eligibility checks on flat-rate claims, so the responsibility to actually qualify for the relief stays with the claimant even without a receipt requirement.

One mistake worth avoiding here: workwear without a visible identifying logo doesn’t qualify, even where a specific colour or style is required by the employer.

Conclusion

A 1263L tax code isn’t good news or bad news by itself. It simply means HMRC has adjusted your tax-free Personal Allowance in the UK to reflect an approved relief or expense. What matters is understanding why that adjustment has been made.

Most of the time, the reason is simple: uniform tax relief, an approved subscription or an automatic change HMRC made on its own. What people often miss is that a tax code doesn’t update itself when things change. A job that no longer needs a uniform can still keep the old code for years.

A quick look at the Personal Tax Account settles it either way. If the code is right, nothing needs to happen. If it’s wrong, sorting it out early keeps a small £60 mistake from growing into a bigger one.

Daniel Wolfson & Co can check a 1263L tax code, confirm whether uniform relief is being applied correctly or handle a backdated claim directly. Call 01923 856 008 or email info@danielwolfson.co.uk to have it reviewed.

FAQs

What does the 1263L tax code mean?

It means the Personal Allowance for that job is £12,630, £60 above the standard £12,570 under 1257L. The letter L confirms the standard allowance applies with nothing else adjusting the calculation.

Why would HMRC give someone a 1263L tax code?

Almost always because a flat-rate expense claim has been approved, most commonly for uniform upkeep. HMRC applies the extra £60 automatically through the tax code rather than as a separate payment.

What is a Notice of Coding?

It’s also called a form P2. It’s the letter HMRC sends whenever a tax code changes, showing what makes up the new allowance. It states the reason in HMRC’s own terminology, such as “flat rate job expenses,” rather than naming uniform relief directly.

What is the difference between 1257L and 1263L tax codes?

The only difference is the amount of Personal Allowance. A 1257L tax code gives the standard £12,570 allowance, while 1263L gives £12,630 after an extra £60 has been added, usually because of uniform tax relief, an approved professional subscription or another eligible adjustment.

How much extra pay does the 1263L tax code actually give?

The £60 difference only changes tax by the amount saved on it, not by £60 itself, roughly £12 a year at basic rate and £24 at higher rate. It shows up as a small monthly difference, not a lump sum.

Does a 1263L tax code carry over automatically after a job change?

Often, yes, since HMRC tends to carry the figure over rather than reset it at a new employer. Whether the relief still applies depends on the new role, not on HMRC checking it for you.

Can uniform relief change my tax code to 1263L?

Yes, if HMRC approves a £60 flat-rate expense for maintaining an eligible work uniform, it may increase the Personal Allowance from £12,570 to £12,630, resulting in a 1263L tax code.

What does the S in S1263L mean?

It means Scottish Income Tax rates apply instead of the rest of the UK’s, since Scotland sets its own tax bands. The allowance itself is identical at £12,630.

Does a falling tax code have anything to do with uniform relief?

No, a falling code usually reflects a benefit in kind or previously unpaid tax being collected, not a change to the Personal Allowance. This explanation only covers a rising code.

Can HMRC change a 1263L code back to 1257L later?

Yes, where HMRC finds the flat-rate expense no longer applies, the code reverts to 1257L and any relief overpaid may be collected through a future coding adjustment rather than a lump sum.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.