The HMRC P11D deadline for the 2025/26 tax year is 6 July 2026. Any UK employer who provided taxable benefits to employees or directors that were not processed through payroll must file P11D and P11D(b) forms electronically by this date and give each affected employee a copy of their information.

If the deadline is missed, HMRC charges penalties automatically from 6 July with no grace period.

This guide explains benefits in kind tax UK rules, employee benefits tax UK obligations and the key P11D submission deadlines employers must meet.

Key takeaways

- P11D and P11D(b) deadline: 6 July 2026. Class 1A NIC is due 22 July (electronic) or 19 July (cheque).

- An incorrect P11D carries a penalty of up to £3,000 per form, separate from the late filing charge.

- Whether a benefit is taxable or exempt depends on how it was provided, not just what it is.

- From April 2025, HMRC reviews the official rate of interest on beneficial loans quarterly, not annually.

- Beneficial loans and living accommodation remain on P11D reporting after April 2027. They are not included in mandatory payrolling.

P11D Submission Deadline 2026: UK HMRC Key Dates

These are the four dates every UK employer should confirm before the end of June.

| Date | What is required |

|---|---|

| 5 July 2026 | Last date to agree a PAYE Settlement Agreement with HMRC for 2025/26 |

| 6 July 2026 | P11D and P11D(b) filed electronically with HMRC. Employee copies provided by the same date. |

| 19 July 2026 | Class 1A NIC payment deadline (cheque) |

| 22 July 2026 | Class 1A NIC payment deadline (electronic) |

Submission is completed through HMRC’s PAYE Online service via Government Gateway using your employer PAYE reference or through recognised commercial payroll software.

Who needs to file and who does not?

Any UK employer limited company, sole trader with employees, charity or owner-managed business must file where taxable benefits were provided to employees or directors that were not processed through payroll during 2025/26.

When you don’t need to file a P11D

Not every employer needs to submit individual P11D forms. You do not need to file if:

- All benefits were fully payrolled if every taxable benefit was reported and taxed through PAYE in real time during 2025/26, individual P11D forms are not required for those benefits.

- No benefits were provided at all if you did not provide any taxable benefits or expenses to any employees or directors during the tax year, there is nothing to report.

One important exception: even if you fall into either category above, you may still need to submit a P11D(b) if Class 1A National Insurance contributions are due including on payrolled benefits. Do not assume that skipping P11D forms means skipping P11D(b).

Once you have confirmed whether you need to file, the next step is understanding which forms are involved and what each one does.

What does each form do?

P11D and P11D(b) are two separate forms that work together. Most employers need to file both.

| Form | P11D | P11D(b) |

|---|---|---|

| What it reports | Taxable benefits and expenses for each individual employee or director | Total Class 1A NIC owed by the employer across all benefits |

| Filed | Once per employee or director who received benefits | Once per employer per tax year |

| Required when | Any taxable benefit was not processed through payroll | A P11D(b) is required if Class 1A NIC is due, including on payrolled benefits. |

| Deadline | 6 July 2026 | 6 July 2026 |

A late or incorrect P11D affects the employee’s tax position, while a late or incorrect P11D(b) affects the employer’s NIC reporting.

How to file a P11D in 2026?

Employers must complete the P11D reporting process before 6 July 2026 to avoid penalties and ensure employees are taxed correctly on their benefits.

The process involves the following steps:

- Identify employees and directors who received taxable benefits that were not payrolled during 2025/26.

- Calculate the taxable value of each benefit using HMRC’s valuation rules.

- Complete a separate P11D form for each employee or director who received reportable benefits.

- Prepare a P11D(b) showing the total Class 1A National Insurance due on all reportable and payrolled benefits.

- Submit the P11D and P11D(b) forms electronically to HMRC by 6 July 2026.

- Provide a copy of the relevant benefit information to each affected employee by 6 July 2026.

- Pay any Class 1A National Insurance due by 19 July 2026 if paying by cheque or by 22 July 2026 if paying electronically.

Employers normally submit P11D and P11D(b) forms electronically using HMRC-compatible payroll software or HMRC’s PAYE Online service. Before submitting, review the checklist below to ensure all required information has been included and nothing has been overlooked.

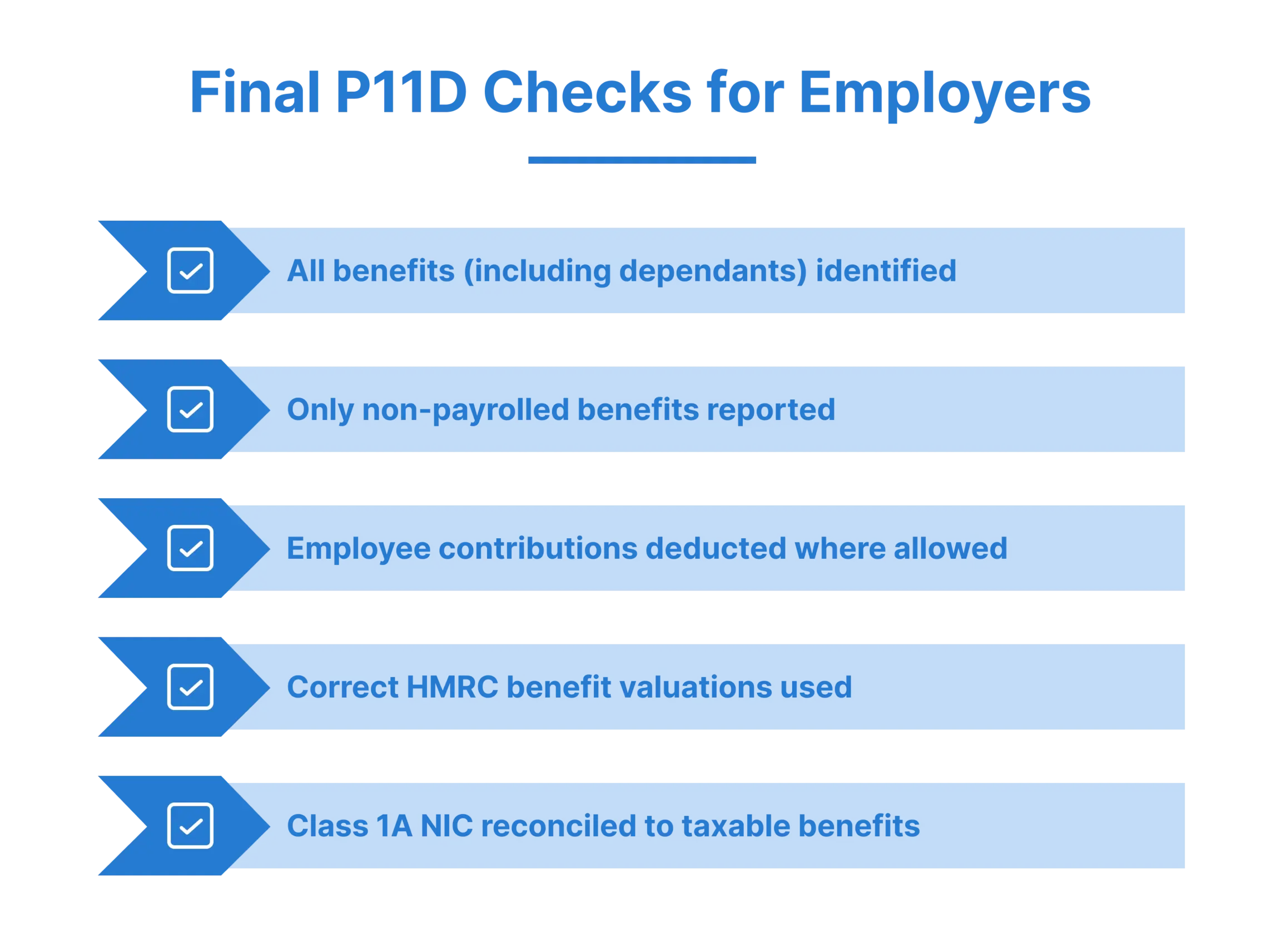

P11D Employer Checklist for 2026

Many P11D errors arise from a small number of recurring issues. Reviewing the points below before filing can help reduce the risk of penalties, additional tax liabilities and HMRC enquiries.

Final P11D Checks for Employers

- All benefits (including dependants) identified

- Only non-payrolled benefits reported

- Employee contributions deducted where allowed

- Correct HMRC benefit valuations used

- Class 1A NIC reconciled to taxable benefits

Completing these checks before submission can help identify issues early and reduce the likelihood of corrections, penalties or compliance queries after filing.

What goes on a P11D?

HMRC does not require every benefit to be reported. The same benefit can be taxable, exempt or conditionally exempt depending on how it was provided. Misclassifying in either direction produces either an incorrect return or an unnecessary tax charge on the employee.

Always reportable if not processed through payroll

| Benefit | Basis of valuation for 2025/26 |

|---|---|

| Company car | List price x CO2-based BIK percentage (3% for zero-emission EVs, up to 37% for high-emission vehicles) |

| Private fuel for company car | Fixed multiplier of £28,200 x same CO2 percentage as the car |

| Company van used privately | Flat rate of £4,020 |

| Private medical or dental insurance | Employer’s premium, including any element covering family members |

| Beneficial loans above £10,000 | Difference between interest charged and HMRC’s official rate of 3.75% for 2025/26 |

| Living accommodation | Assessed under HMRC’s accommodation valuation rules |

| School fees, personal bills, gym memberships | Cost to the employer |

Exempt benefits (no P11D required)

Trivial benefits of £50 or less are exempt provided the benefit is non-cash, not a reward for performance and not contractual. Directors of close companies cannot receive more than £300 in trivial benefits per tax year. Employees have no such limit, only the £50 per-item condition.

Other exempt benefits include one employer-contracted mobile phone per employee, cycle to work equipment, employer pension contributions, one annual health check and business expenses reimbursed at HMRC-approved rates.

Conditionally reportable

Some benefits may be taxable or exempt depending on how they are provided, including:

- Homeworking payments.

- Relocation expenses.

- Training costs.

- Certain vouchers and allowances.

HMRC decides whether a benefit is taxable based on why it was given. For example, a £45 gift for a birthday is usually exempt, but the same gift given as a performance reward becomes fully taxable.

How are benefits valued and where errors occur?

The cash equivalent on the P11D is not always the cost to the employer. Each benefit has a specific HMRC valuation method and applying the wrong figure produces an incorrect return.

For example, a director receives:

- Company car benefit: £9,920

- Private medical insurance: £1,800

Total reportable benefit: £11,720

At a Class 1A NIC rate of 15%, the employer would owe £1,758 in Class 1A NIC.

Valuation errors are more common than late filing errors and the penalty is heavier. Three areas account for most of them.

Making good

Any amount an employee pays towards a benefit reduces the cash equivalent pound for pound. Contributions not recorded result in an overstated P11D value and excess Class 1A NIC.

Beneficial loan rate changes

HMRC now reviews the official rate quarterly. If the rate changed mid-year, the benefit must be calculated separately for each period. A single rate applied across the full year will produce an incorrect figure.

PHEV easement

HMRC introduced a temporary easement for plug-in hybrid vehicles registered between 1 January 2025 to 5 April 2025. For qualifying vehicles, the CO2 figure is treated as 1g/km for BIK purposes. Employers who have not applied this may have overstated the liability.

These three valuation errors also appear consistently in HMRC compliance checks, along with a number of other common mistakes that employers tend to overlook until they receive a compliance letter.

Common HMRC Mistakes on P11D Returns

Valuation errors are not the only issue HMRC finds during compliance checks. The following mistakes are also common and can lead to additional tax, Class 1A NIC liabilities and penalties.

- Reporting payrolled benefits on a P11D

If a benefit has already been taxed through payroll, reporting it again on a P11D can result in the employee being taxed twice on the same benefit. - Leaving out benefits provided to family members

Benefits such as private medical or dental insurance that cover a spouse or dependants must be reported based on the full cost paid by the employer. - Getting company car calculations wrong

Common errors include using the wrong CO₂ emissions percentage, not applying available reliefs for plug-in hybrid vehicles or failing to adjust the benefit when the car was only available for part of the tax year. - Not deducting employee contributions

Where employees contribute towards a benefit, that contribution should be taken into account. If it is missed, the taxable benefit and Class 1A NIC may be overstated. - Using one beneficial loan rate for the entire year

HMRC now reviews official rates quarterly. Using a single annual rate may produce incorrect results if the rate changed during the year. - Misunderstanding trivial benefits rules

A gift is not automatically tax-free just because it costs less than £50. If it is given as a reward for performance or forms part of a contractual arrangement, it may still be taxable. - Not submitting a P11D(b)

Some employers assume that payrolling all benefits removes the need for a P11D(b). However, a P11D(b) is still required where Class 1A NIC is due.

Each of these mistakes can create additional costs for employers, which is why understanding HMRC’s penalty rules is so important.

Penalties for Late Filing and Incorrect Returns

HMRC operates two separate penalty regimes for P11D. Most employers are only aware of one.

Late Filing of P11D(b)

A penalty of £100 per 50 employees or part of 50 applies for every month or part month the P11D(b) remains unfiled after 6 July. There is no grace period and the charge accumulates until the form is submitted.

Incorrect P11D

Penalties for an inaccurate return can reach £3,000 per form, additional to any late filing charge.

A miscalculated car benefit, a missed family medical premium or a loan assessed at the wrong rate can each produce an inaccuracy penalty that far exceeds the late filing cost. This is the charge most employers are unaware of until an HMRC compliance letter arrives.

Late Payment of Class 1A NIC

Interest applies from 23 July 2026. Additional percentage-based penalties can follow on unpaid amounts.

Keeping a clear record of how each benefit was valued, with supporting figures for each calculation, is the most practical defence against an HMRC compliance check.

How Payrolling Changes P11D Reporting from April 2027 (HMRC Plans)

From 6 April 2027, the government plans mandatory payrolling for most benefits in kind, with loans and living accommodation remaining exceptions at the outset. Individual P11D forms will be abolished for payrolled benefits, but P11D will still be needed for loans and accommodation.

Beneficial loans and living accommodation are excluded from mandatory payrolling initially. HMRC has confirmed P11D reporting for both continues beyond April 2027. Employers who assume all P11D obligations end after 2026/27 will remain non-compliant.

One transition risk that is frequently not planned for: when an employer moves to payrolled benefits, employees may have tax collected on the previous year’s benefits through their tax code and on the current year’s benefits through payroll at the same time.

This creates a temporary reduction in take-home pay that employees need to be told about in advance.

Conclusion

The 6 July 2026 deadline covers filing and employee copies. The 22 July deadline covers payment of Class 1A NIC. Missing either has a direct financial cost.

The returns most likely to contain errors are not always the complex ones. A benefit placed in the wrong category, a contribution not recorded or a loan rate applied incorrectly each produces an inaccuracy penalty that most employers do not anticipate.

If any part of your 2025/26 benefits reporting is uncertain or you want to ensure your business is prepared for the April 2027 transition, professional support before the deadline is far more manageable than a correction after it.

A final review before filing can help reduce errors, penalties and employee tax issues.

To get your P11D return prepared and filed accurately before 6 July 2026, contact Daniel Wolfson & Co on 01923 856 008 or email office@danielwolfson.co.uk.

FAQs

Does a P11D need to be filed if all benefits were payrolled in 2025/26?

No, individual P11D forms are generally not required for benefits that were properly payrolled. However, employers must still submit a P11D(b) by 6 July 2026 if Class 1A National Insurance contributions are due on those benefits.

What is the official rate of interest for beneficial loans in 2025/26?

HMRC’s official rate of interest for beneficial loans is 3.75% (subject to quarterly review). Employers using the actual method should check the applicable rate for each quarter when calculating the taxable benefit.

Can directors of close companies receive trivial benefits?

Yes, but the £300 per tax year limit applies to the director personally as a total, not per benefit. Multiple gifts can collectively breach the limit even if each one individually cost under £50.

Does an employee contribution towards a benefit reduce the P11D value?

Yes, any amount an employee pays towards a benefit reduces the taxable value reported on the P11D pound for pound. The reduction only applies if the payment is made to the employer, not to a third party such as an insurance provider directly.

Are beneficial loans and living accommodation included in mandatory payrolling from April 2027?

Loans and living accommodation are expected to remain outside mandatory payrolling at the start, so employers should check HMRC’s latest guidance. Employers may still be able to payroll these benefits voluntarily, but final rules should be confirmed.

What is the deadline to agree a PAYE Settlement Agreement for 2025/26?

The agreement must be in place with HMRC before 5 July 2026. One-point employers often miss is that a PSA only covers benefits that are minor, irregular or impractical to apportion individually. Benefits that do not meet these conditions must be reported on a P11D or processed through payroll.

What happens if a P11D or P11D(b) is filed late?

HMRC may charge penalties for late filing and interest on late Class 1A National Insurance payments. Additional penalties can apply if the information submitted is inaccurate or incomplete.

Can a P11D be amended after submission?

Yes, if an error is identified after filing, employers can submit an amended P11D and where necessary, a corrected P11D(b) to ensure HMRC records are updated.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.