Most businesses that register for VAT remain on Standard VAT accounting unless they choose an alternative scheme, such as the Flat Rate Scheme. Most stay there without reviewing whether a different approach would suit them better.

The Flat Rate Scheme exists as a formal alternative, but it is widely misunderstood some businesses that would benefit from it never apply and others continue using it long after it no longer fits their position.

The scheme a business uses affects how VAT is calculated each quarter, how much record-keeping is involved and in some cases the actual VAT outcome. That difference is not always visible until the numbers are compared against the specific cost structure of the business.

This article explains how both schemes work in practice, what separates them and what the decision should actually be based on, including the factors most comparisons do not cover.

Key takeaways

- Standard VAT requires businesses to subtract input VAT from output VAT each quarter and pay or reclaim the difference from HMRC.

- The Flat Rate Scheme applies a fixed sector percentage to gross VAT-inclusive turnover, ranging from 4% to 14.5%.

- Limited Cost Traders, those spending less than 2% of VAT-inclusive turnover on qualifying goods or under £1,000 a year, whichever is higher, must use a flat rate of 16.5%.

- Input VAT cannot be reclaimed under the Flat Rate Scheme, except on individual capital assets costing over £2,000.

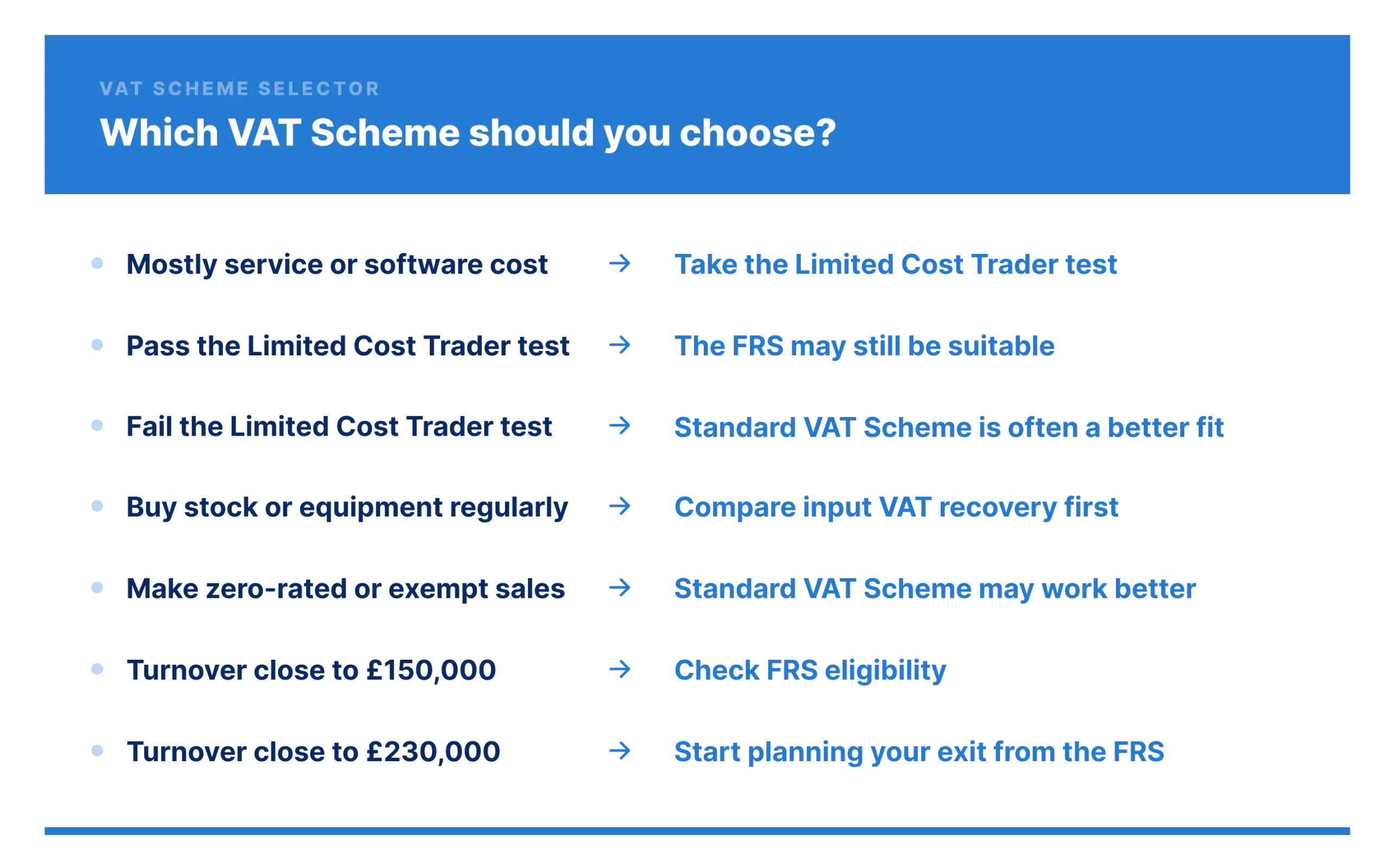

- A business must leave the Flat Rate Scheme when VAT-inclusive turnover exceeds £230,000 in the past 12 months or is expected to in the next 12 months.

If turnover has exceeded £230,000 but is expected to fall below £191,500 in the following 12 months, HMRC may allow the business to remain on the scheme. This requires written application and HMRC agreement it is not automatic.

How Standard VAT Accounting works in practice?

Standard VAT Accounting gives businesses full control over what they pay. Every quarter, a business charges VAT on its sales and pays VAT on its purchases. The difference between the two is what goes to HMRC or comes back from it.

What the calculation involves:

The VAT charged on sales is output VAT. The VAT paid on business purchases is input VAT. When output exceeds input, the business pays the difference to HMRC. When input exceeds output, HMRC issues a repayment.

Every qualifying purchase feeds into that reclaim stock, equipment, software, professional fees, marketing cost and subcontractor invoices where VAT has been charged. For businesses with significant VATable cost, that reclaim is real money returned every quarter.

Who benefits most from input VAT recovery:

Standard VAT produces its strongest advantage for businesses with consistent, meaningful VATable expenditure. This includes:

- Businesses purchasing stock regularly

- Businesses investing in equipment

- Businesses paying for software licences and cloud tools

- Businesses using VAT-registered subcontractors

- Businesses making a mix of standard-rated, zero-rated or exempt sales

That last category matters for a specific reason. Where a business sells across different VAT rate categories, Standard VAT reflects the actual position accurately. A flat calculation cannot do that.

The administration trade-off:

Every purchase and sale invoice must be recorded and reconciled throughout the quarter. Accurate bookkeeping records are what make the return correct. For businesses with minimal VATable purchases, this raises a reasonable question about whether the reclaim justifies the workload.

That question is what the Flat Rate Scheme was designed to answer, but the answer is not always what businesses expect.

How the Flat Rate Scheme works in practice?

The Flat Rate Scheme replaces the output-minus-input calculation with a single fixed percentage applied to gross turnover. Whether that simplification produces a better outcome depends entirely on what the business gives up in exchange.

How the calculation works:

For standard-rated sales, invoices still include VAT at 20%, so nothing changes at the customer-facing level. The difference lies in how the VAT return is calculated. Instead of separating output VAT and input VAT, the business applies a fixed percentage to its total VAT-inclusive turnover based on its HMRC-defined sector and pays that amount to HMRC.

HMRC publishes the full list of flat rate percentages by business type, ranging from 4% for retailers of food, confectionery, tobacco, newspapers or children’s clothing to 14.5% for accountants and IT consultants. The applied rate is lower than the standard VAT charged on sales, which is why a portion of the VAT collected is effectively retained by the business.

For example, a photographer charging £1,000 plus £200 VAT generates £1,200 in gross turnover. With a flat rate of 11%, the VAT due is £132. The remaining £68 represents the difference between VAT collected from the customer and VAT paid to HMRC, which is where the scheme creates its financial effect.

What the first-year discount changes:

Businesses in their first year of VAT registration receive a 1% reduction on their applicable flat rate.

The 12-month discount window is measured from the VAT registration date, not the date of joining the scheme. A business that joins FRS after registering for VAT loses whatever portion of that window has already passed.

For newly registered businesses, this discount is worth factoring into any comparison at the point of registration.

The capital assets exception

VAT on individual capital assets costing over £2,000 can still be reclaimed separately on the VAT return for the period in which the purchase was made. This exception is frequently overlooked by businesses already on the scheme.

The Flat Rate Scheme cannot be used with the separate Cash Accounting Scheme. It has its own cash-based turnover method for businesses that account on a receipts basis, which works similarly but operates under different rules.

Businesses often focus on the sector percentage when evaluating FRS. The financial outcome depends just as much on the input VAT that would have been recoverable under Standard VAT. For many businesses, that figure is larger than expected.

The calculation looks straightforward on paper. Whether a business can actually use it depends on meeting HMRC’s conditions first.

Eligibility and Scheme Rules for the Flat Rate Scheme

Joining the Flat Rate Scheme is not automatic. HMRC sets specific conditions, and a business that does not meet them cannot apply, regardless of how favourable the sector rate looks.

Who can join:

A business can join the Flat Rate Scheme if its expected VAT taxable turnover in the next 12 months is £150,000 or less, excluding VAT. The business must already be VAT-registered, or be applying for VAT registration at the same time as applying for the scheme.

When a business cannot join:

Several conditions exclude a business from joining, even where the turnover test is met:

- The business left the Flat Rate Scheme in the previous 12 months

- The business has committed a VAT offence, such as a penalty for VAT evasion, in the previous 12 months

- The business is closely associated with another business already using the scheme, where combined turnover exceeds the threshold

- The business is, or within the past 24 months has been, registered for VAT as part of a VAT group or eligible to join an existing VAT group treatment

How to apply:

A business can join the Flat Rate Scheme online at the same time as registering for VAT, or by submitting form VAT600FRS separately. HMRC confirms acceptance through the business’s VAT online account, or by post if the application was not made online.

Joining after VAT registration

A business does not need to join the Flat Rate Scheme at the point of VAT registration. It can apply later, provided it still meets the eligibility conditions. The 1% first-year discount, however, only applies for the 12 months following the VAT registration date. Joining later in that window reduces how much of the discount period remains.

Meeting the conditions only confirms access to the scheme. What it actually costs to use becomes clear once input VAT is removed from the equation.

The Limited Cost Trader rule: Who it catches and why it matters?

Not every business on the Flat Rate Scheme pays its sector rate. For a significant number of small service businesses, a separate classification overrides it entirely and most are unaware it applies until the numbers are checked.

What the classification means:

A business is a Limited Cost Trader if its spending on qualifying goods falls below either 2% of its VAT-inclusive turnover or £1,000 per year, whichever is higher. When this applies, the business pays 16.5% regardless of its sector.

HMRC provides a checker tool to assess the limited cost business rate for each return period.

What counts as qualifying goods:

The definition is narrower than most businesses assume.

Goods that qualify:

- Physical goods purchased for use in the business

- Stock bought for resale

- Stationery and printer paper

- Materials and physical supplies

Goods that do not qualify:

- Software and cloud subscriptions

- Travel and fuel

- Subcontractor cost

- Professional services fees

- Rent and premises cost

Why service businesses are most at risk:

A consultant spending £150 per month on physical supplies but £700 per month on software has qualifying goods spend of £1,800 per year. At a turnover of £100,000, the 2% threshold is £2,000. The consultant falls short and pays 16.5%, not the sector rate.

At 16.5%, the margin between collected VAT and paid VAT is minimal. For most service businesses at that rate, FRS produces no meaningful advantage over Standard VAT.

Many businesses that joined FRS several years ago passed the goods test comfortably at the time. As spending shifted toward software and services, they became Limited Cost Traders without realising it. The checker should be used at every return period, not just at the point of joining.

The flat rate is one part. The bigger cost is often the input VAT you cannot recover.

What the Flat Rate Scheme removes from Standard VAT?

The Flat Rate Scheme removes input VAT reclaim on day-to-day purchases. For businesses with low cost, this is a minor consequence. For businesses with regular VAT-eligible expenditure, it is the most significant financial feature of the scheme.

What is permanently lost:

Under Standard VAT, you recover VAT on all qualifying purchases (software, fees, office cost, phone, marketing, subcontractors). Under FRS, none of that is recoverable – it becomes a permanent cost.

The capital assets exception applies only to individual items over £2,000. Multiple smaller purchases cannot be combined to reach the threshold. Each item is assessed on its own.

For example:

For a business spending £2,000 per quarter on VATable purchases, that is £400 of input VAT absorbed into cost every quarter under FRS. Over a full year, that is £1,600 that Standard VAT would return.

Whether the flat rate produces a better outcome depends on whether the margin retained under FRS exceeds the input VAT lost. That comparison requires actual figures, not assumptions.

For some businesses, the fixed rate produces a favourable outcome even after accounting for the lost reclaim. For others, FRS gradually becomes one of the most expensive ways to account for VAT, particularly as the business grows and its cost base expands.

The right scheme is the one that cost less, net of everything. The next section shows how that plays out across different business types.

Which scheme fits which Business?

The scheme decision relies on three variables: cost structure, purchase frequency and the mix of sales. The table below compresses the core differences before the scenarios apply them.

| Key consideration | Standard VAT | Flat Rate Scheme |

|---|---|---|

| Calculation method | Output VAT minus input VAT | Fixed % of gross VAT-inclusive turnover |

| Input VAT recovery | Full reclaim on qualifying purchases | Not available (capital assets over £2,000 excepted) |

| Administration load | Higher all invoices tracked | Lower single percentage applied |

| Suits best | High-purchase and mixed-supply businesses | Low-overhead service businesses not classified as Limited Cost Traders |

| Risk area | VAT repayment delays | Limited Cost Trader classification, lost input VAT |

Low-overhead service business

A consultant, designer or freelancer with cost primarily in time and expertise will have limited input VAT to reclaim under Standard VAT. If the applicable sector rate is below 20% and the business is not a Limited Cost Trader, FRS may produce a retained margin each quarter.

The Limited Cost Trader test must come first. If the business fails it, the 16.5% rate makes Standard VAT the more appropriate option in most cases.

Product-based or stock-purchasing business

A retailer or wholesaler buying stock regularly generates significant input VAT each quarter. Under Standard VAT, stock VAT is fully recoverable. Under FRS, you cannot reclaim it: it stays as a cost.

For limited companies and businesses in product-led sectors, Standard VAT almost always produces a better outcome once input VAT reclaim is factored in. The administration saving from FRS does not offset the VAT cost at meaningful purchase volumes.

Business selling zero-rated or exempt goods

Food retailers, booksellers and children’s clothing businesses charge no output VAT on their primary sales. Under Standard VAT, they pay no output VAT on those sales and still reclaim input VAT on purchases.

Under FRS, the flat rate applies to all gross turnover, including turnover from zero-rated or exempt sales. The business pays VAT on sales where it collected none from customers. Standard VAT gives accurate control here. FRS does not.

The three scenarios cover the most common positions. The checklist below brings them into a single decision view.

For most businesses, the scheme decision is clear once the cost structure is examined. What is less obvious is that the right answer today may not hold as the business grows.

When to leave the Flat Rate Scheme?

Joining FRS is not a permanent decision. The scheme has mandatory exit thresholds and the responsibility for monitoring them sits entirely with the business. HMRC does not issue reminders.

The thresholds that require action:

A business must leave the Flat Rate Scheme when any of the following apply:

- VAT-inclusive turnover in the past 12 months has exceeded £230,000

- VAT-inclusive turnover is expected to exceed £230,000 in the next 12 months

- VAT-inclusive turnover is expected to exceed £230,000 in the next 30 days alone

A business that remains on FRS past either threshold is filing incorrect VAT returns. Full details of the conditions for leaving the Flat Rate Scheme are on GOV.UK.

Once a business leaves the scheme, it cannot rejoin for 12 months. Voluntary exit is also available at any time, which becomes relevant when the scheme no longer produces a favourable outcome.

When to reassess before reaching the threshold:

Several situations should prompt a scheme review before turnover thresholds become relevant:

- Annual accounts completion

- A large equipment purchase approaching £2,000

- A significant change in turnover trajectory

- Taking on VAT-registered subcontractors

- A change in primary business activity affecting the sector rate

Any of these can shift whether FRS remains appropriate. The threshold conditions are the point at which the business must act. These triggers are the point at which it should think.

The thresholds explain one category of error. The more common mistakes happen long before a business reaches them.

Common mistakes with VAT scheme decisions

Most VAT scheme errors do not happen at registration. They develop gradually as the business changes and the scheme does not.

- Applying the wrong sector rate: Where a business spans more than one activity, the rate should reflect the primary one. Applying a rate from a secondary activity produces an inaccurate return, regardless of intent.

- Never repeating the Limited Cost Trader check: Many businesses run the check once at joining and do not return to it. Cost structures change and a business that qualified at one stage may have become a Limited Cost Trader since. The checker should be used at every return period.

- Staying on FRS past the exit threshold: Turnover growth can move a business past the £230,000 VAT-inclusive threshold without anyone noticing mid-year. Quarterly monitoring is necessary, not annual.

- Missing the capital assets reclaim: Businesses on FRS regularly overlook the exception for individual assets over £2,000. The reclaim is not automatic it must be claimed on the VAT return for the period in which the purchase was made.

- Not comparing schemes against actual figures: Many businesses choose FRS because it sounds simpler, without comparing it against actual input VAT spend. For some, the comparison clearly favours FRS. For others, Standard VAT would recover more than the flat rate retains.

- Choosing a scheme at registration and never reviewing it: A decision that made sense at £60,000 turnover may not hold at £130,000. Cost structures, subcontractors, equipment and software spend all change as a business grows.

- Assuming simpler bookkeeping = lower VAT liability: FRS reduces admin, but it does not automatically reduce VAT. If your input VAT under Standard VAT would be higher than the margin FRS keeps, then simpler records actually cost you more.

Conclusion

Both VAT schemes have a logic, but that logic only holds under the right conditions. Standard VAT gives full input VAT recovery and accurate control over mixed-supply positions. The Flat Rate Scheme reduces administration but removes that recovery and its value depends entirely on cost structure, sector rate and whether the Limited Cost Trader rule applies.

Businesses often review their VAT scheme when registering for VAT, approaching the Limited Cost Trader threshold or noticing that their cost profile has changed. In those situations, reviewing the calculation before a return is submitted can confirm whether the current scheme remains appropriate.

Daniel Wolfson & Co helps businesses identify the right VAT scheme from the point of registration, manages scheme changes with HMRC and handles quarterly VAT returns accurately. To discuss your VAT position, call 01923 856 008, email office@danielwolfson.co.uk or visit the VAT accounting services page.

Can I join the Flat Rate Scheme after VAT registration?

What counts as goods for the Limited Cost Trader test?

What happens if I become a limited cost trader?

Do I still need to keep VAT records on the Flat Rate Scheme?

Can I reclaim VAT on equipment under the Flat Rate Scheme?

What is the first-year FRS discount and when does it apply?

Should a growing business stay on the Flat Rate Scheme?

What happens if I apply the wrong flat rate sector percentage?

When should I ask an accountant to review my VAT scheme?

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.