The Seed Enterprise Investment Scheme (SEIS) is a UK government scheme that gives investors up to 50% income tax relief when they invest in early-stage startups. It also includes capital gains tax exemption and loss relief, which reduces the financial risk of backing a business that is still in its early stages.

For UK startups, this makes a real difference when raising early funding. Investors have a clear financial reason to back a business at its earliest stage, not just belief in its potential.

This guide covers how SEIS works, who qualifies, what relief investors receive and how founders can use it as part of their funding strategy in 2026.

Key Takeaways

- Investors can claim back 50% of their SEIS investment against their income tax liability.

- Any gain on SEIS shares held for three or more years is free of capital gains tax.

- A startup can raise a maximum of £500,000 under SEIS (increased from £250,000 from April 2025).

- The company must have been trading for less than three years, fewer than 25 full-time equivalent employees and gross assets no more than £350,000 immediately before the share issue.

- Directors can invest in their own company under SEIS, which is not permitted under EIS.

- SEIS and EIS cannot be used in the same accounting period. SEIS shares must be issued before any EIS or VCT investment in that period.

- The compliance process after investment typically takes around 14 weeks.

How SEIS Tax Relief Works for Investors

SEIS tax relief is claimed by the investor, not the company. For founders, understanding the mechanics is important, as investors will look for clarity on how the relief applies before they invest.

Income Tax Relief

Investors can claim back 50% of their SEIS investment against their income tax liability.

On a £20,000 investment, that is £10,000 back from HMRC. The maximum SEIS investment per investor per tax year is £200,000, giving a maximum SEIS income tax relief of £100,000.

Investors can also carry this relief back to the previous tax year, which gives flexibility on when it is claimed.

Capital Gains Tax Relief and Loss Relief

If an investor holds SEIS shares for at least three years and income tax relief has not been withdrawn, any gain on disposal is free of capital gains tax. There is no upper limit on the qualifying gain.

SEIS reinvestment relief allows investors to apply a 50% CGT exemption on gains reinvested into SEIS shares, up to £100,000.

If the company fails, SEIS loss relief applies to the net loss after income tax relief has been accounted for. The real financial exposure ends up significantly lower than the amount originally invested.

Example:

An investor puts £20,000 into a SEIS-qualifying startup. SEIS income tax relief of 50% reduces their effective cost to £10,000. If the company fails and they subsequently claim SEIS loss relief at 45%, they recover £9,000 on their £20,000 loss. The real loss is just £1,000, making SEIS one of the most investor friendly tax reliefs available.

That shift in risk profile is what makes SEIS investment a fundamentally different proposition from an investment that carries no tax relief.

SEIS Eligibility: Company and Investor Conditions

Both the company issuing shares and the individuals investing must meet their respective SEIS qualifying criteria for relief to apply.

Company Requirements

To issue SEIS shares, a company must satisfy all of the following at the point shares are issued:

- The company must be UK-incorporated or have a permanent UK presence

- It should be trading for less than three years at the time the shares are issued

- It must have fewer than 25 full-time equivalent employees

- Gross assets should not exceed £350,000

- The company must not be listed on a recognised stock exchange

- It cannot be a subsidiary of, or controlled by, another company

- It must not have received prior funding under EIS or from a Venture Capital Trust (VCT)

- The funds raised must be used for qualifying business activities within three years

The Risk to Capital Condition

Introduced by HM Revenue & Customs in 2018, this is a mandatory requirement for SEIS.

To qualify, the business must:

- Have genuine plans to grow over the long term

- Involve real risk for investors, with no guaranteed or protected returns

HMRC will assess your business plan, how funds are used and whether any arrangements reduce investor risk. If investors have priority rights, early exit options or built-in protection, the condition is unlikely to be met.

The aim is simple: SEIS should support genuine business growth, not low-risk tax-driven investments.

Qualifying Trades

The SEIS scheme is open to most commercial businesses, but HMRC excludes specific sectors.

Excluded trades include property development, financial and banking services, legal and accountancy services, farming, forestry, leasing, most energy generation, hotels, nursing homes and shipbuilding.

Software, technology, life sciences, engineering, manufacturing and consumer products all fall clearly within the SEIS qualifying trades. If your business operates in any of the excluded sectors, confirm your position before approaching investors.

Rules for Investors

Individual UK taxpayers can invest under SEIS, provided they hold no more than 30% of the company’s total shares and are not employees of the company.

Directors can invest under SEIS and claim full relief, provided they hold no more than 30% of shares, voting rights or rights to assets. Under EIS, directors who control the company (over 30%) are excluded from relief, but non-controlling directors can invest and claim.

For founding teams where personal capital is part of the raise, this is an important distinction.

HMRC typically responds to advance assurance applications within 4 to 6 weeks. For time-sensitive funding rounds, apply at least 8 weeks before your target investment date.

Preparing for a SEIS Raise

Getting to the point of issuing shares involves two practical stages: securing advance assurance from HMRC before investment and running the compliance process after shares are issued.

Advance Assurance

SEIS advance assurance is confirmation from HM Revenue & Customs that your proposed share issue is likely to qualify. It is not a guarantee, but most investors expect it before committing.

The application is submitted to HMRC’s Venture Capital Reliefs team and typically includes a business plan, financial forecasts, details of the share issue and any previous investment.

HMRC reviews your financial position as part of this process, so clear and accurate records help avoid delays. Having your accounts and structure in order before applying makes the process much smoother.

How to Claim SEIS Tax Relief: The Compliance Process

Once shares are issued and SEIS funding is in place, a compliance process allows investors to claim their SEIS tax relief.

Before filing, the company must either have been trading for four months or have spent at least 70% of the SEIS funds raised.

There is also a filing deadline. The company must notify HMRC using form SEIS1 within two years of the share issue date. If missed, investors may lose their SEIS income tax relief.

The process then follows four steps:

- The company files a compliance statement (SEIS1) with HMRC, confirming all SEIS rules have been met and listing the investors requesting certificates.

- HMRC reviews and issues a SEIS2 letter with a unique reference number, authorising the issue of investor certificates.

- The company issues a SEIS3 certificate to each investor using that reference number.

- Each investor uses their SEIS3 to claim SEIS income tax relief through Self Assessment or via their PAYE tax code.

From share issue to investors receiving their SEIS3 certificates, the process typically takes around 14 weeks.

The Difference Between SEIS and EIS

The Seed Enterprise Investment Scheme (SEIS) and the Enterprise Investment Scheme (EIS) are UK government schemes that help startups attract investment by offering tax relief to investors. The key difference is the stage at which they apply.

SEIS is for very early-stage companies. It applies to businesses under three years old with gross assets up to £350,000 and offers 50% income tax relief.

EIS comes later, once the business has grown. It allows larger funding rounds and offers 30% tax relief.

In most cases, startups raise SEIS first and then move to EIS as they scale. Once a company uses EIS, it cannot go back and use SEIS, so the order matters.

From April 2025, EIS investor limits were increased from £1m to £1.5m (general) and £2m to £3m (knowledge-intensive), making it easier for growing companies to raise larger amounts

| Aspects | SEIS | EIS |

|---|---|---|

| Income tax relief | 50% | 30% |

| Investor annual limit | £200,000 | £1,500,000 (£2m for knowledge-intensive) |

| Company maximum raise | £250,000 | £10m per year (£20m knowledge-intensive) |

| Company age limit | Under 3 years | Up to 7 years |

| Employee limit | Fewer than 25 | Fewer than 250 |

| Gross asset limit | Under £350,000 | Under £30m |

| Directors can invest | Yes | Generally no |

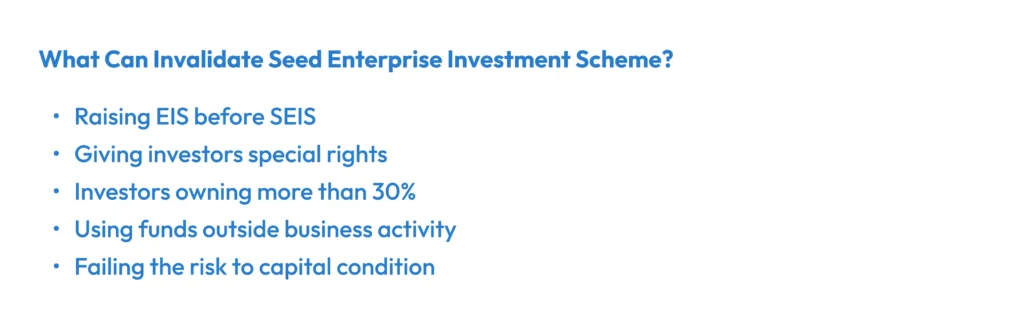

Mistakes That Affect SEIS Eligibility

Most SEIS problems are avoidable. These are the ones that come up most often.

- Receiving EIS or VCT Funding Before SEIS: Once EIS or VCT investment has been received, SEIS is no longer available. The sequencing is fixed and cannot be corrected after the fact.

- Including Ineligible Investors: Employees of the company cannot be SEIS investors. Investors holding more than 30% of shares do not qualify. Including either in the compliance statement can invalidate the relief for the whole raise.

- Issuing Shares with Preferential Rights: SEIS shares must be ordinary, full-risk shares. Any preferential rights to assets or income beyond a limited dividend preference will disqualify the investment.

- Misusing SEIS Funds: Funds must be used for the qualifying business activity within three years of the share issue. Spending outside that scope or failing to meet the deadline can trigger clawback.

- Clawback within the Three-Year Holding Period: If the company ceases to meet SEIS rules within three years of the share issue, through a change of trade, an acquisition or a stock market listing, HMRC withdraws the SEIS income tax relief from investors, who must then repay it.

Note: The SEIS maximum qualifying investment limit (£500,000) and the Income Tax basic rate threshold (£50,270) remain in place for 2026-27. Unlike the £1,000 Personal Allowance freeze, SEIS limits have not been increased further since April 2025

Conclusion

SEIS is a practical funding tool for UK startups at the seed stage. The SEIS tax relief it offers investors is substantial and for many founders, having SEIS advance assurance in place is what moves a funding conversation forward.

The process works best when the company is properly prepared. Accurate financial records, a correctly structured company and accounts that reflect the trading position clearly all contribute to a smoother SEIS advance assurance application and a cleaner compliance process after investment.

If you are building a UK startup and want to make sure your accounts and company structure are in good shape before approaching investors, Daniel Wolfson & Co works with early-stage businesses at exactly this stage. Call 01923 856 008 or email office@danielwolfson.co.uk to book a consultation.

Frequently Asked Questions

What is SEIS and how does it work?

SEIS gives UK investors 50% income tax relief, CGT exemption after three years and loss relief, reducing the financial risk of investing in early-stage UK companies.

What are the SEIS eligibility conditions for a company?

The company must be UK-incorporated, trading for less than three years, have fewer than 25 employees, gross assets under £350,000 and no prior EIS or VCT funding.

Do I need SEIS advance assurance before approaching investors?

No, it is not required, but most investors expect it, as it confirms HMRC believes your share issue is likely to qualify for SEIS.

Can a founder or director invest in their own SEIS company?

Yes, directors can invest and claim SEIS relief, provided they do not hold more than 30% of shares, voting rights or company value.

What if we raise less than the amount in advance assurance?

SEIS relief applies only to the amount actually raised, so you do not need to meet the full amount stated in your advance assurance.

Can non-UK investors join a SEIS round?

Yes, they can invest, but they cannot claim SEIS tax relief, as income tax relief, CGT exemption and loss relief are limited to UK taxpayers.

Can SEIS tax relief be taken back?

Yes, if SEIS rules are breached within three years or shares are sold early, HMRC can withdraw the relief and require repayment.

What is the risk to capital condition?

The company must aim for long-term growth and investors must face a real risk of loss, as guaranteed returns or protection will disqualify SEIS.

What is the SEIS1 filing deadline?

You can apply after four months of trading or using 70% of funds and must file within two years of the share issue date or investors lose tax relief.

Can SEIS shares have special rights?

No, SEIS shares must be ordinary with no preferential rights, as guaranteed returns or priority payouts will invalidate the relief.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.