Choosing between salary and dividends is one of the most important decisions for limited company directors and shareholders in 2026-27. While many directors take a combination of both, but the right balance depends on your company’s profits, your tax position and how you want to withdraw income from the business.

The way you pay yourself affects your personal tax, National Insurance and the company’s tax bill.

As tax rates and thresholds keep changing, it is worth reviewing whether the way you pay yourself is still the most tax efficient.

Key takeaways

- For many limited company directors, a salary of £12,570 with dividends from remaining profits is a common approach, though the right salary can vary depending on your Employment Allowance position

- Dividends carry no National Insurance from either side making them more tax-efficient than salary above the Personal Allowance

- Dividend tax rates increased by 1.25 percentage points from 6 April 2026, bringing the basic rate to 10.75% and the higher rate to 35.75%

- Dividends must come from distributable profits only, not from the bank balance

- Dividend income is not taxed through PAYE and must be declared via Self-Assessment by 31 January 2028

How are Salary and Dividends taxed differently?

Salary and dividends are both taxable, but they are treated differently. The main difference is that salary carries National Insurance, while dividends do not.

That difference is what makes the combination more efficient than either option used on its own.

Salary

Salary goes through payroll. Income tax applies on earnings above £12,570 and National Insurance applies from both sides, 8% from you on earnings between £12,570 and £50,270 and 15% from the company on earnings above £5,000.

That is a combined NI burden of 23% in the basic rate band before income tax is counted. A director’s salary is also a deductible business expense reducing the company’s Corporation Tax bill by 19% to 25%.

The 8% employee NI applies on earnings between £12,570 and £50,270; the 15% employer NI applies on earnings above £5,000. These do not all apply simultaneously on the same amount of income.

Dividends

Dividends come from the company’s post-tax profits. Unlike salary, they do not have National Insurance for either the individual or the company.

The first £500 each year is free under the Dividend Allowance. Any amount above that is taxed at dividend rates which are lower than income tax rates.

| Band | Income Range | Salary | Dividends |

|---|---|---|---|

| Personal Allowance | Up to £12,570 | 0% | 0% |

| Basic Rate | £12,571 to £50,270 | 20% | 10.75% |

| Higher Rate | £50,271 to £125,140 | 40% | 35.75% |

| Additional Rate | Above £125,140 | 45% | 39.35% |

Then why is salary still important?

If you only take dividends, the company does not get Corporation Tax relief on that income and do not build up a qualifying year for your State Pension as dividends are not part of your National Insurance record.

Taking a salary above £6,708 helps secure that qualifying year and reduces the company’s taxable profit. If the salary stays within the Personal Allowance, there is usually no Income Tax or employee National Insurance to pay.

What is the most tax-efficient Director’s salary in 2026/27?

For most directors it is £12,570 but the correct figure depends on whether your company qualifies for the Employment Allowance.

Sole director and no other employees

If the director is the only employee on the payroll. A company where the director is the only employee cannot claim Employment Allowance. This means Employer National Insurance applies at 15% on salary above £5,000.

Even with that cost, the salary still works in the company’s favour. Because a director’s salary is a deductible business expense, it reduces taxable profit and generates a Corporation Tax saving at either 19% or 25% depending on the company’s profit level.

Since the Corporation Tax saving rate exceeds the Employer NI rate of 15%, the deduction produces a net benefit in most cases. The exact position depends on the company’s profit and tax rate.

Second employee above the secondary threshold

A company with a second employee paid above the Secondary Threshold can claim the Employment Allowance of £10,500.

This eliminates the Employer NI liability entirely in most cases, which means the full Corporation Tax saving on the salary flows through with no extra NI cost.

At £12,570 the salary qualifies for full Corporation Tax relief as a deductible expense at no NI cost to the company.

How the pay mix actually looks?

A director taking £12,570 as salary and the remaining income as dividends can often reduce the overall tax bill.

The salary can be taken without paying Income Tax or employee National Insurance, while dividends above the £500 Dividend Allowance are taxed at 10.75% for basic rate taxpayers.

The right balance depends on company profits and total income, so it is worth reviewing the figures to make sure the split still fits your situation.

Can Shareholders who are not Directors receive Dividends?

Yes, and each shareholder is entitled to their own Personal Allowance and Dividend Allowance regardless of whether they draw a salary.

A spouse or family member holding shares can receive company dividends without being on the payroll. Each shareholder has their own Personal Allowance of £12,570 and £500 Dividend Allowance so someone with no other income can receive up to £13,070 before any personal tax is due.

Passive shareholders and spouse investors

A spouse or partner holding shares but playing no active role is still entitled to dividends in line with their shareholding. Across two shareholders, the combined household allowance is £26,140 before basic rate dividend tax applies.

These arrangements are legitimate, but HMRC applies the settlements legislation where shares appear to have been issued purely to redirect income. Professional advice is recommended before making any shareholding changes.

Multiple share classes (alphabet shares)

Some companies issue different share classes, often labelled A, B and C, allowing different dividend amounts to be paid to different shareholders without changing the ownership split. The structure is legal but HMRC will challenge it where no commercial rationale exists.

Can a shareholder waive a dividend?

Yes, a shareholder can sign a deed of waiver before a dividend is declared. The waived amount stays in the company as retained profit and is not taxable for the waiving shareholder. The waiver must be in place before declaration, properly documented and commercially justified.

Interim and Final Dividends

Directors can declare interim dividends at any point during the year provided distributable profits exist at that time.

Final dividends are declared after year end once the full profit position is confirmed and typically require shareholder approval. Both types carry the same documentation requirements.

The two-company rule and the settlements legislation

If you receive dividends from two separate limited companies HMRC combines both streams under your single personal tax position. A director receiving £20,000 from Company A and £20,000 from Company B does not benefit from two separate Dividend Allowances or basic rate bands. Both are added together and taxed as one.

Directing dividends toward a connected person is legitimate when the shareholding reflects a genuine commercial arrangement.

HMRC applies the settlements legislation, rules that counteract arrangements where income is redirected to a connected person with no real business basis behind the structure. Professional advice is needed before any shareholding changes are made.

What does paying Dividends correctly actually require?

A dividend is only valid if the company has sufficient distributable profits at the time it is declared, not just a positive bank balance.

Distributable profits are accumulated realised profits less accumulated realised losses under section 830 of the Companies Act 2006.

Directors who pay dividends based on available cash and find at year end that Corporation Tax liabilities have reduced distributable profit below what was paid out will have the excess reclassified as a director’s loan.

How to check if you have enough distributable profits?

Take your retained earnings from the most recent accounts. Deduct dividends already paid this year and an estimate of the Corporation Tax liability not yet recorded. What remains is your available distributable profit. Do not declare a dividend above that figure.

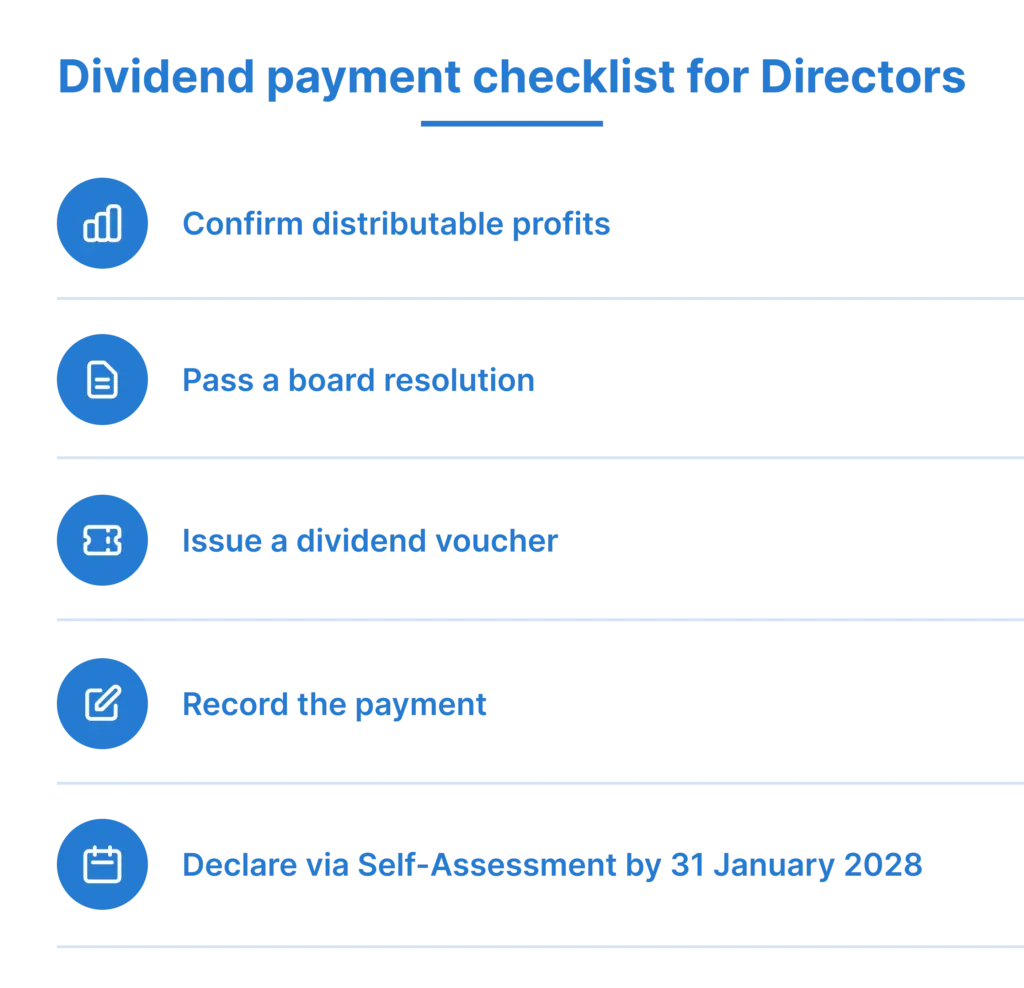

- Prepare or update management accounts to confirm distributable profit is sufficient

- Hold a board meeting and pass a resolution approving the dividend

- Issue a dividend voucher to each shareholder showing the date, company name, shareholder name and amount per share

- Make the payment and record it in the company’s books

- Each shareholder declares the income via Self-Assessment

This process applies to both interim and final dividends. Skipping any step, particularly the board resolution or voucher can leave the dividend open to challenge.

What happens if it goes wrong?

- Any director’s loan above £10,000 on which no interest is charged at HMRC’s official rate creates a Benefit-in-Kind charge, which must be reported through P11D.

- A loan outstanding nine months and one day after year end is subject to a Section 455 charge of 35.75% on the due balance, increased from 33.75% on 6 April 2026 in line with the dividend upper rate.

- Under section 847 of the Companies Act 2006 a shareholder who knew or should have known the dividend was unlawful is personally liable to repay it.

The correct process

Before each dividend is declared the company needs up-to-date management accounts confirming distributable profit, a board resolution approving the payment and a dividend voucher recording the date, company name, shareholder name and amount.

Every dividend declaration must follow this process without exception.

Any dividend paid outside this process risks being reclassified as a director’s loan.

What has changed from April 2026?

Three things: Dividend tax rates rose by 2%, the Secondary Threshold stayed at £5,000 and both main allowances remain frozen until at least April 2028.

- Dividend tax rates increased from 8.75% to 10.75% at the basic rate and from 33.75% to 35.75% at the higher rate from 6 April 2026. For a basic rate taxpayer taking £30,000 above the allowance that is around £590 more in tax this year.

- The Secondary Threshold remains at £5,000 following its reduction from £9,100 in April 2025. For sole directors without the Employment Allowance every pound of salary above this figure costs the company 15% before it reaches you, which is why the Employment Allowance question carries more weight this year.

- The Personal Allowance and Dividend Allowance remain frozen at £12,570 and £500 until at least April 2028. As earnings grow and thresholds stay fixed more directors move into the higher rate band each year without adjusting anything about how they structure their pay.

How does Dividend Income get reported to HMRC?

It does not go through payroll. Any amount above the £500 Dividend Allowance must be declared through Self-Assessment and the filing and payment deadline for 2026/27 is 31 January 2028.

Directors not yet registered for Self-Assessment need to do so well before that date. HMRC does not chase dividend tax through PAYE the responsibility sits with the individual to declare and pay it correctly.

When do Pension Contributions make more sense than extra Dividends?

For directors already in the higher rate band at 35.75% an employer pension contribution is often more tax-efficient than taking the same amount as a dividend.

A contribution paid directly from the company reduces taxable profit. The Corporation Tax saving is between 19% and 25% depending on company profit levels. It carries no National Insurance and does not count as personal taxable income so no dividend tax applies on it either.

The numbers at higher income levels

For a director with total income of £55,000 redirecting £5,000 into a pension rather than taking it as a dividend saves 35.75% dividend tax on that amount plus the Corporation Tax relief on the contribution, a combined saving considerably greater than extracting the equivalent as a dividend.

For directors with income approaching £100,000 pension contributions reduce adjusted net income, which is total income minus contributions and certain reliefs. The Personal Allowance tapers once this figure exceeds £100,000 and disappears entirely at £125,140. A pension contribution can restore part of that allowance producing a saving beyond the Corporation Tax relief.

The annual pension allowance for 2026/27 is £60,000. Any unused allowance from the previous three tax years 2023/24, 2024/25 and 2025/26 can be added on top of this, provided the director was a member of a registered pension scheme in each of those years. This allows a larger pension contribution in a more profitable year.

Conclusion

The salary vs dividends question is not a one-time decision. The right salary level, Employment Allowance position, correct dividend process and whether pension contributions make better use of higher-rate profits all shift as the business grows and tax rules change.

For most limited company directors and shareholders in 2026/27 a £12,570 salary combined with dividends from remaining profits remains the most tax-efficient structure. The April changes have made the detail more consequential, frozen thresholds and higher dividend tax rates mean more directors are paying more than necessary without realising it.

Daniel Wolfson & Co advises limited company directors and shareholders across North-west London on remuneration planning, year-end accounts and personal tax returns. Call 01923 856 008 or email office@danielwolfson.co.uk to speak with the team.

Frequently Asked Questions

Can a director take dividends if they are not a shareholder?

No, dividends can only be paid to shareholders based on the shares they own, so a director who does not hold shares in the company cannot receive dividends.

Can I take dividends if my company made a loss this year?

Dividends can still be paid if the company has enough retained profits from previous years, but if there are not enough distributable profits, the company should not pay them.

Does taking dividends affect a mortgage application?

Yes, it can, as many lenders look more closely at salary than dividend income when deciding how much they are willing to lend, which can affect directors who take a low salary and higher dividends.

Do dividends affect Statutory Sick Pay or Maternity Pay?

Yes, these payments are based on PAYE salary only, and dividend income is not included, so a salary above the Lower Earnings Limit of £6,708 is usually needed to qualify.

What is marginal relief and why does it matter?

Marginal relief applies when company profits fall between £50,000 and £250,000, where the Corporation Tax rate gradually increases from 19% to 25%, and in this range, paying a salary can help reduce the company’s taxable profit.

Does the salary and dividends split differ for Scottish directors?

Dividend tax rates are the same across the UK. However, the Scottish higher rate of 42% begins at £43,663 rather than £50,270, which changes the point at which dividends become more tax-efficient than salary.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.